The State of Our Economy: Republicans Are Saying One Thing, Democrats Another… and Both Have “Facts” to Prove Their Claims

Here’s What I Think

On Aug.16 and Aug. 23, I wrote about the key issues I believe we’ll be hearing about from Trump/Vance and Harris/Walz for the next two and a half months.

My argument was that the issues that are most important to core Trump voters and core Harris voters – such as immigration, rising crime, gender ideology, and censorship on one side, and abortion, trans rights, global warming, and the plight of the Palestinians on the other side – won’t be the deciding factors in the upcoming election.

Instead, as it has so many times before, it will come down to the economy. To be more accurate, to the perception of the economy by undecided voters in the swing states.

So, is it healthy – perhaps healthier than it’s been in years – as Harris has recently been claiming? Or is it, as Trump is suggesting, a skyscraper of debt and mismanagement teetering on the verge of collapse, but savable if he is in the Oval Office?

I am not an economist. What I know about economics is the result of heading up a business that has been publishing newsletters, books, and special reports on investing for more than 30 years.

Nevertheless, I’m going to tell you what I’m thinking right now based on the reading I’ve done in the past, the ups and downs I’ve experienced as a businessman, and what I’ve been studying over the past several weeks to write this piece.

Here’s the Good News

The good news is that, despite countless predictions by some doomsayers to the contrary, the US economy has not fallen into a depression. In fact, we are not even in an official recession.

GDP has been growing a bit faster than expected, inflation growth is, at least temporarily, ebbing, and job opening numbers are officially rising.

Consumers are spending less, which is good, However, these same consumers are borrowing more – which Biden administration economists interpret as stimulating for the economy, though others see it as bad.

That’s all I could find for the good news. If you think I missed anything, please let me know.

And Here’s the Not-Good News

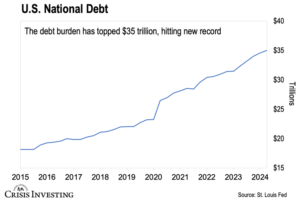

At the top of the not-good news is that the US is now about $35 trillion in debt, which is about $105,000 for every individual and $270,000 for every US household.

Over the last 12 months, as you can see above, the national debt has surged by nearly $2.3 trillion. That’s about $6.4 billion every single day, roughly $266.7 million an hour, and around $4.44 million a minute.

Click here if you want to watch it tick up live by the second. But be warned – it’s disturbing.

I know these numbers are abstract and difficult to fathom. But stick with me as I try to explain, to the best of my understanding, why they are so scary.

This peak debt of $35 trillion is not only an all-time high for the US, but also more than twice the debt load of China (in second place at about $14 trillion), almost three times Japan’s (in third place at about $13 trillion), and more than 10 times the UK’s (in fourth place at about $3 trillion).

$35 trillion is about 125% of our GDP, the sum of all the goods and services we produce. This is bad. Not as bad as Japan’s and Italy’s debts as a percentage of GDP, at 250% and 140% respectively, nevertheless bad.

As I said, the US economy is not in a recession right now. (A recession is technically defined as a fall in GDP for two successive quarters.) But for the US to avoid a recession in the near future, the Fed must reduce its $7.2 trillion balance sheet and stay on a path to normalize monetary policy. That is going to be a difficult – maybe impossible – job. It’s likely, in fact, that the Fed will restart “quantitative easing” – i.e., printing more dollars – very soon. That will increase, not reduce, our debt.

As for inflation, the Labor Dept.’s CPI (Consumer Price Index) rose 2.9% year-on-year in July, the smallest gain since 2021. That is a fact the Harris camp will be using.

According to official government data, inflation, which is most often calculated by using the CPI, advanced only 0.2% in July, up 3.2% year-on-year. But this is misleading.

That official rate, now called “core inflation,” does not include the cost of energy and food, which, quite obviously, comprise very significant percentages of middle-class and working-class expenses. And while it’s true that prices for some goods have fallen, they have been more than offset by rising prices for a range of items, including auto insurance (18.6%), childcare (5.1%), fast food (4.3%), and internet services (3.9%).

As for job growth, the Harris campaign is claiming that US employers added 114,000 jobs in July and taking credit for that as a sign of a recovering economy. What they won’t tell you is that the US economy must produce at least 150,000 new jobs each month just to keep up with population growth. So even if we did add 114,000 jobs last month, we would still be losing ground.

And it’s worse than that. These job growth numbers are estimates that have been consistently and grossly inflated. Here’s an explanation of how overblown the government’s numbers have been over the last 12 months.

From the WSJ:

It isn’t difficult to get a positive employment report every month when you are “adjusting” the final number by about a quarter of a million jobs that you just “assume” are being created somehow.

In any event, even if we take the government’s report at face value, the Sahm Rule (which has successfully predicted every recession since 1970) has still been officially triggered…. The rule stipulates that a recession is likely when the three-month moving average of the jobless rate is at least a half-percentage point higher than the 12- month low.

Over the past three months, the unemployment rate has averaged 4.13%, which is 0.63 percentage points higher than the 3.5% rate recorded in July 2023.

But Enough with the Government’s Questionable Data –

Let’s Look at What Is Happening in Reality

I feel more comfortable interpreting numbers that are easier to understand and harder to fake – i.e., numbers reported by businesses that are required under penalty of law to be correct. And here, the overall outlook is bleak.

Some examples:

Banking

US banks closed 28 branches across the country in just one week in July. Wells Fargo, Bank of America, and US Bank each closed eight locations in the last week. Greenville Fed, Chase, and Schaumberg Bank & Trust closed the other four.

Retail Business

The retail industry is going through a tough time. Since the COVID shutdown, there has been a massive abandonment of businesses across the country. Thousands of mom-and-pop stores have closed – many in urban areas – and retail chains are in no better shape.

The surveys I’ve looked at say the great majority of the mom-and-pops are shut for good. And those closed chain stores – it’s hard to say, but it is going to take time and some divine intervention to grow the economy to the point where they will be reopened.

If it were just the smaller stores, it would be bad news but not necessarily reflective of the health of the retail industry at large. However, these smaller closures are happening at the same time as the big ones.

Some examples:

* Two months after announcing plans to close about 40 stores nationwide due to financial woes, Big Lots has indicated on its website that it intends to close almost 300.

* Macy’s has plans to close more than 150 of its stores over the next three years.

* Stop & Shop will be closing 32 of its large grocery stores in the US northeast “as part of the company’s efforts to improve its financial performance.”

* CVS, one of the US’s largest drugstore chains, closed nearly 900 stores from 2020 to 2024. Additionally, the company announced plans to close dozens of its pharmacies inside Target stores.

* The furniture retailer Malouf sells beds and bedding in a fraction of the colors it did a few years ago.

* Avon Products, once one of the most iconic brands in the beauty industry, filed for Chapter 11 bankruptcy on Aug. 14.

* Blink Fitness, a chain of gyms that has more than 100 locations in seven states announced that it filed for Chapter 11 bankruptcy on Aug. 12.

* The Body Shop, a beauty brand originally from the UK, closed down all its US stores last year.

* In March, Dollar Tree announced that it would be shutting down nearly 1,000 stores in the near future.

* Family Dollar announced that it is planning to close at least 600 stores this year.

* Best Buy, the retail giant specializing in electronics, closed about 24 stores last year. While the company saw strong sales in the last quarter (thanks to the holiday season), it plans to close an additional 10-15 stores by 2025.

* And Walgreens, the big daddy of pharmacy retailers, is projected to shutter 2,150 of its roughly 8,600 locations over the next three years.

Restaurants

Restaurants could be said to be a subdivision of the retail industry, but their financial health is not always in sync. One might hope for some better activity with the restaurant chains – but overall, it’s just more bad news.

For example:

* Applebee’s is closing more than 30 stores this year.

* Red Lobster is closing at least 48 of its stores.

* Bloomin’ Brands began closing some of its Outback Steakhouses in February and plans to continue to close more as needed, as well as other brands it owns, such as Bonefish Grill, Carrabba’s Italian Grill, and Fleming’s Prime Steakhouse.

Overall, at least 11 retail brands have said that they’re closing US stores in 2024, totaling up to 1,401 locations.

Energy

The US has always had the advantage of massive in-ground stores of oil, coal, and natural gas.

Leftists generally and “renewable energy” devotees have been waging a political war against fossil fuels with cultish commitment. The Biden administration, starting on day one, catered to these voters by implementing a series of measures that has made our core energy resources dramatically more expensive in the last three years – which is the argument that Trump and Vance are going to be making.

But I don’t think most Americans from either side of the political spectrum have any idea about the economics of energy or how large the impact of energy prices is on the health of the economy. So, while I do think Biden’s policies have been detrimental to the economy, I don’t think the energy argument will be a winning one for Trump/Vance.

In fact, I’m bullish on oil, gas, and natural gas. I don’t foresee a future where the fossil fuel industry goes bust. Quite the contrary, the harder the government presses to move away from fossil fuels, the more fossil fuels will be consumed between now and whenever a deadline for eliminating them is pursued.

Keep in mind that every technology we have today that is green requires the burning of fossil fuels to produce the hardware and software needed to achieve a green economy.

Utilities

Because of our government’s energy policies over the last several years, utility customers across the country are increasingly paying more for less-reliable service. And the massive heat wave the US has been experiencing this summer has only made the situation much worse.

Real Estate

The US real estate industry is a mess. It began with the hysteria-inducing government-imposed COVID shutdown… which led to tens of millions of office workers working from home… which led to a huge spike in office vacancies and a big drop in commercial real estate prices, which has not been recorded and probably never will.

Example: A Washington, DC, office building was sold at a massive 75% discount last week. The 175,000 sq. ft. tower, which sold for $60 million in 2006, sold for $16 million this time.

Meanwhile, the housing market is falling apart because prices have been inflated so severely over the past several years.

One result is that evictions are on the rise. Eviction filings in 10 cities across the country are up more than 15% over the past year compared with the period before the COVID-19 pandemic began, according to the Eviction Lab, a research unit at Princeton University.

Education

The price to attend a traditional four-year college has surged. Some private colleges and universities recently announced tuition of $90,000+ for the 2024-25 school year.

Families are facing a record amount of student loan debt, with an estimated $100 billion in new loans to be issued in 2024, up from $98 billion in 2023.

That is probably why, according to the WSJ, enrollment at US community colleges focused on vocational skills rose 16% in 2023 to its highest level since 2018, according to National Student Clearinghouse data.

Bankruptcies

Personal and business bankruptcy filings rose 16.2% in the 12-month period ending June 30, 2024, compared with the previous year.

According to statistics released by the Administrative Office of the US Courts, bankruptcy filings totaled 486,613 in the year ending June 2024, compared with 418,724 the previous year. Business bankruptcy filings rose 40.3%, from 15,724 to 22,060 in the year ending June 30, 2024. Non-business filings rose 15.3% to 464,553, compared with 403,000 the previous year.

The Big Picture

The rise of US debt and the dismal state of the US economy cannot be assigned solely to Biden and Harris. The Trump administration – and every other administration in the past 20 years – has been equally complicit. Over that period, the landscape of the US economy changed greatly. The rich have gotten richer. The middle class has gotten poorer. And the number of people reliant on government assistance to survive has exploded.

This gets me back to the beginning of this essay. Wealthy East and West Coast voters may very well believe the economic “facts” they are hearing from the Biden administration and the Harris campaign. But according to a research report I cut and pasted from CBS Money Watch:

* Americans have a specific annual income in mind for what it would take to feel financially secure, according to a new survey from the personal finance site Bankrate. The magic number? $186,000 per year.

* Currently, only 6% of US adults make that amount or more. The median family income falls between $51,500 and $86,000, according to the latest federal data.

* For most Americans, financial security means being able to pay your bills while having enough left over to make some discretionary purchases and put money away for the future – and they have an even higher yardstick for feeling rich. The survey found they believe they would need to earn $520,000 a year to qualify as wealthy – up from $483,000 in the same survey last year.

As Sarah Foster, an analyst at Bankrate, pointed out, that gap between what the typical American earns and what they aspire to earn means “Americans think they need to make more money even if they know it’s unrealistic, they’ll never make that amount.”

Conclusion

Trump is essentially right in pointing out that the US economy is in bad shape – and could be teetering on the brink of collapse. I don’t know if he means it. I don’t even know if he understands macroeconomics. But the same can be said of most American voters.

What matters to voters is the microeconomics of the micro-economies in which they live. And those economies (all the industries listed above) are either floundering or foundering.

I don’t know any company owner or CEO who is optimistic about the future of his business. Nor do I know any consumer that believes prices haven’t risen to frightening heights.

If the November election comes down to how undecided voters feel about the economy today, as opposed to how they felt four years ago, the outcome looks bad for Harris.